The Year at a Glance

IRCC entered 2025 targeting 437,000 study permits issued and 305,900 new student approvals, a managed 10% reduction from 2024. The reality proved far more uneven: approval rates collapsed in several high-volume markets, extensions consumed far more cap space than projected, and new student pipelines are now at generational lows.

What follows is a data-first look at how 2025 actually unfolded, with year-over-year comparisons to 2024, a West Africa spotlight, and the institutional and provincial breakdowns that matter most to Canadian DLIs.

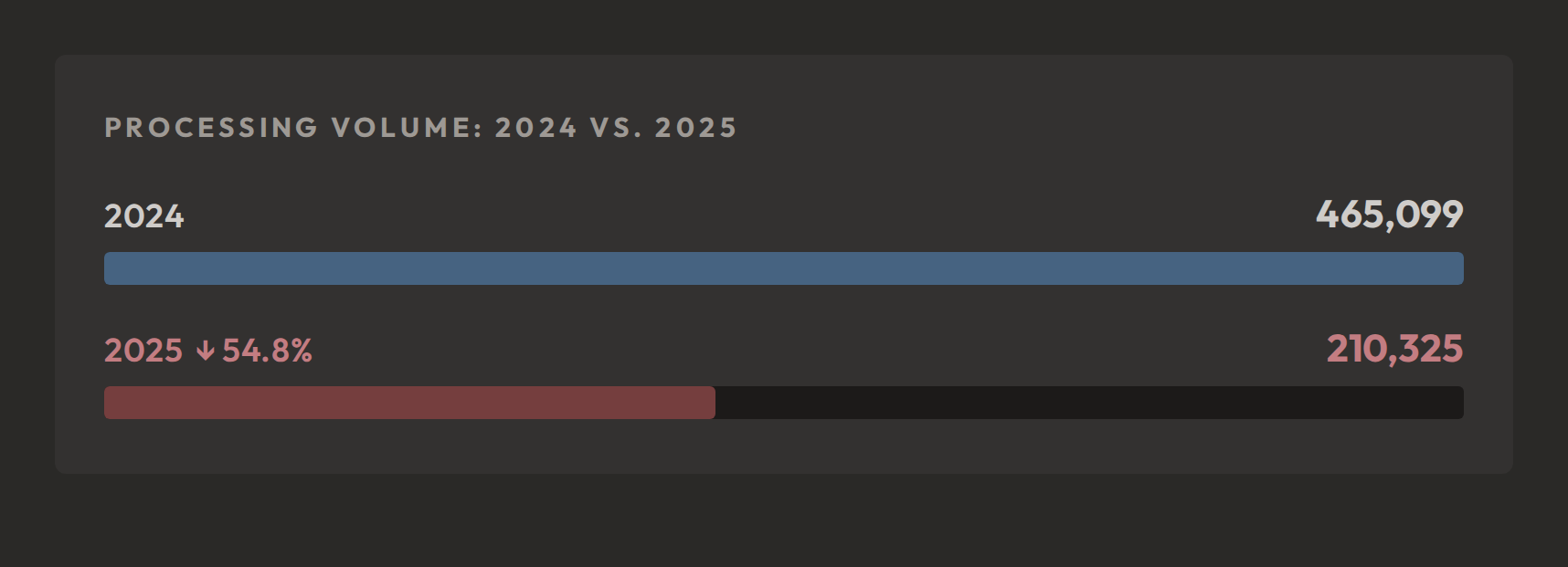

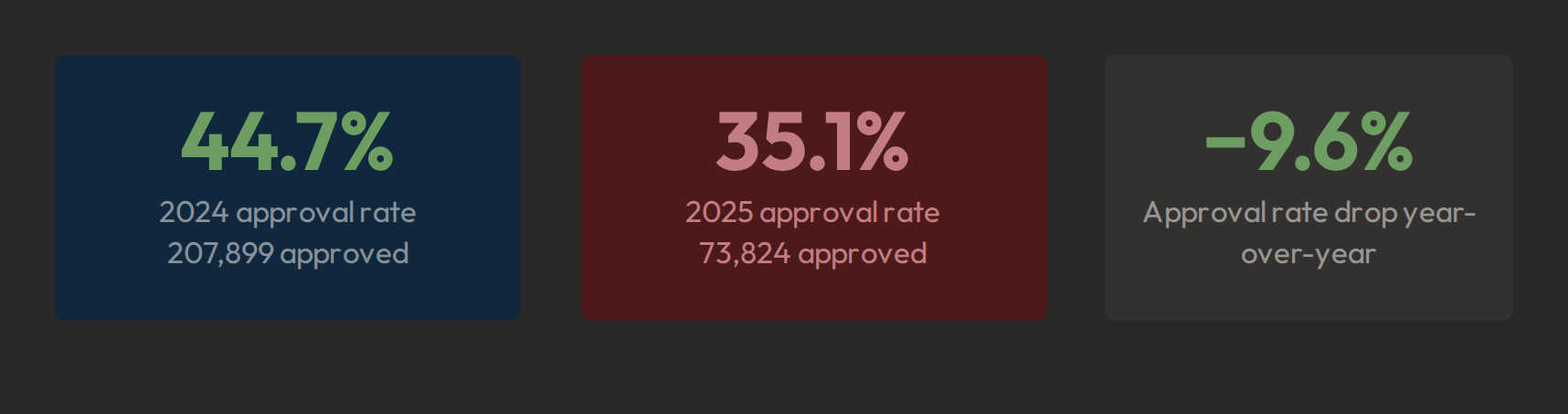

The headline figures tell the story clearly. Processing volumes dropped by nearly half from 2024, approval rates fell across most source markets, and new student inflows landed far below government targets.

IRCC projected 305,900 new student approvals for 2025. Full-year processed data puts actual new permit approvals at approximately 73,800, just 24% of the government's own target. Extensions consumed far more cap space than anticipated, and total new application submissions dropped by nearly 55% year-over-year. The 437,000 total permits cap is being sustained almost entirely by students already in Canada extending their stay.

134,000 fewer approvals in 2025 than in 2024

Even accounting for the intentional cap reduction, the drop from 207,899 approvals in 2024 to approximately 73,824 in 2025 far exceeds what policy alone explains. Lower application volumes, tighter officer discretion, and declining applicant profiles across key source markets all contributed.

The structural shift is real and self-reinforcing

Extensions now account for over 60% of all study permits issued, triple IRCC's original estimate. As fewer new students enter Canada in 2025, the pool of potential future extension applicants shrinks for 2026 and beyond, compounding enrollment challenges for DLIs across every province.

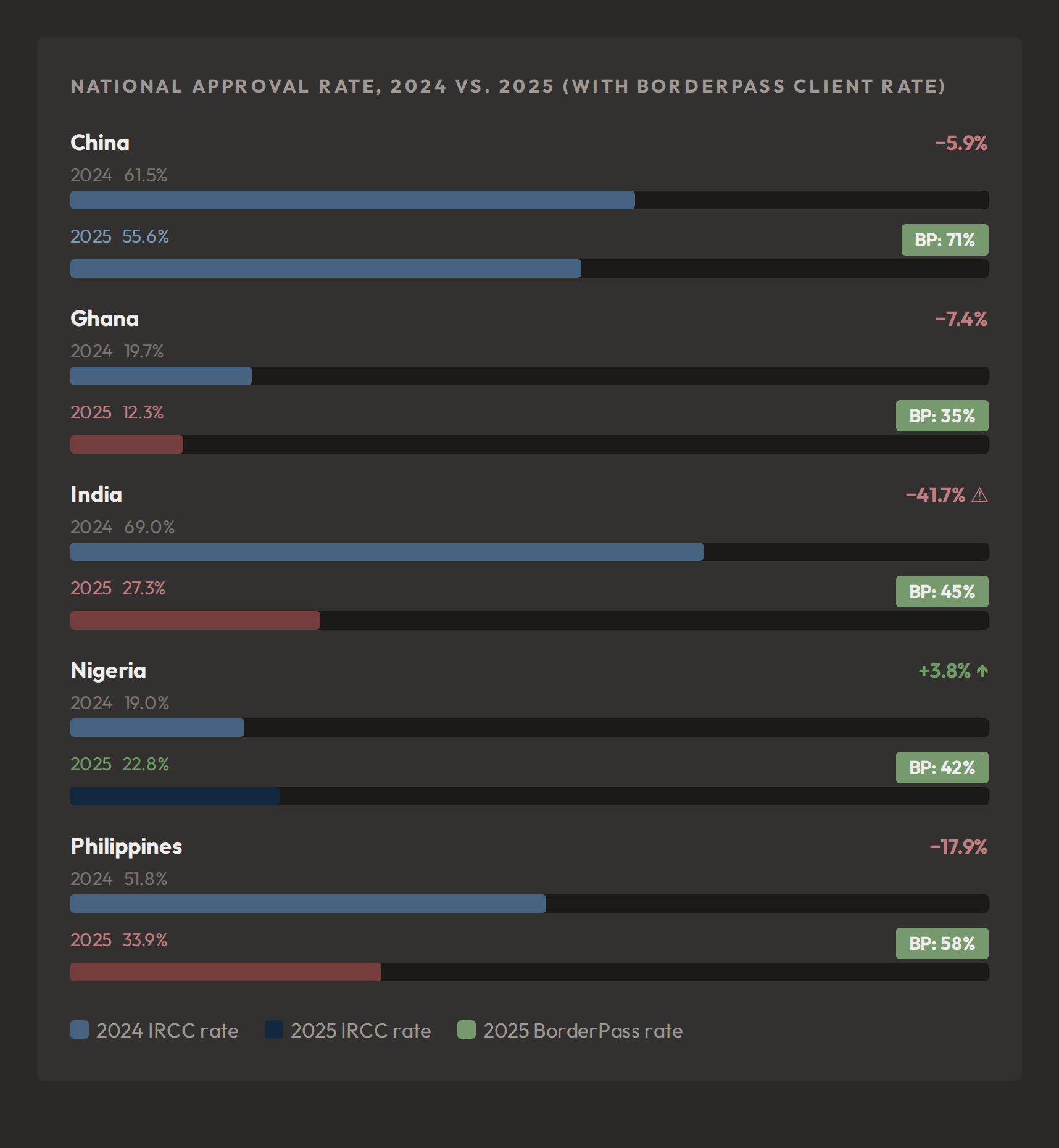

The Five Markets DLIs Rely on Most: 2024 → 2025

Listed alphabetically, these five countries are most central to Canadian DLI recruitment. Nigeria is the only market in this group where the national approval rate improved year-over-year. India's collapse is the most consequential story in the sector.

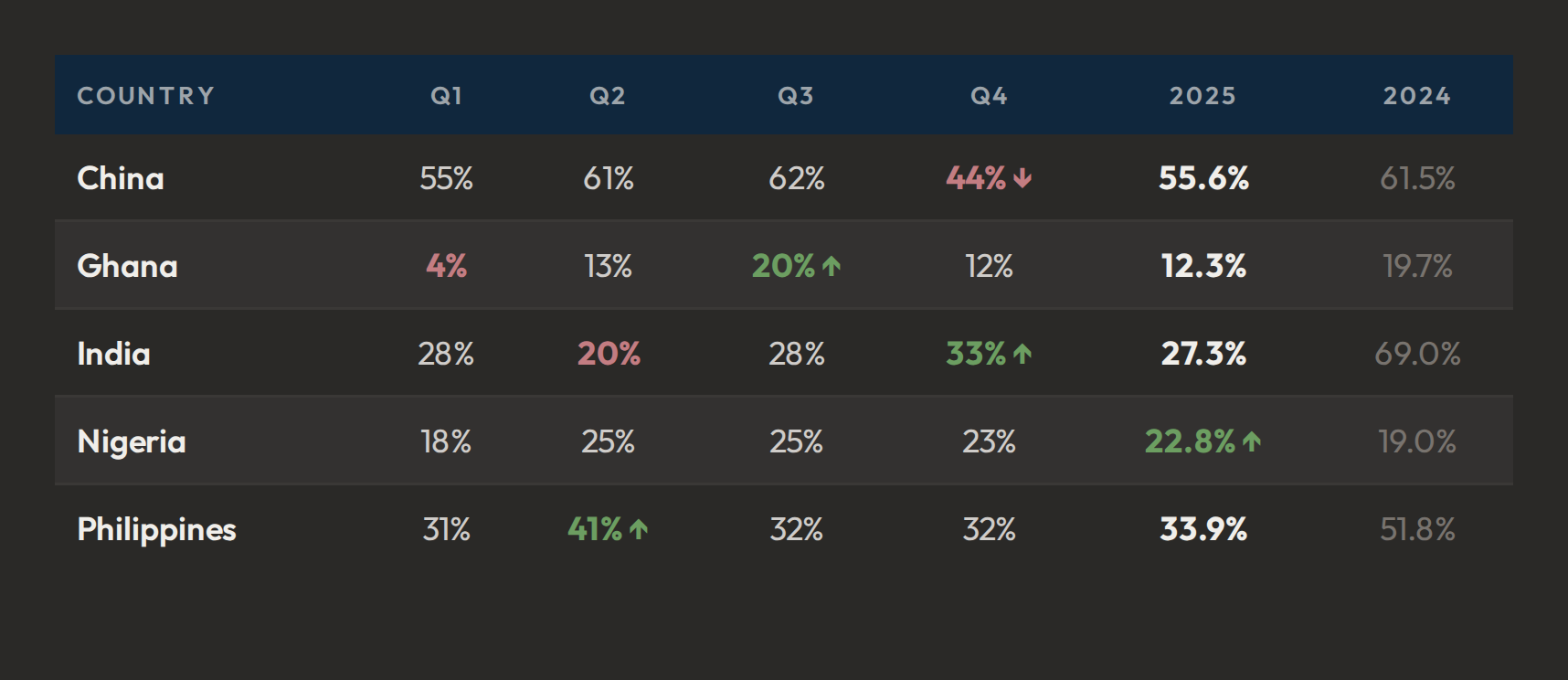

India's 41.7-point drop is the defining story of 2025

India went from 69% in 2024 to 27.3% in 2025, the steepest year-over-year collapse of any major source country. India did close the year on a positive note with Q4 reaching 33%, suggesting early-stage recovery heading into 2026.

Nigeria is the only one of the five to improve year-over-year

A 3.8-point gain, from 19.0% to 22.8%, is modest in absolute terms but signals a positive directional shift. BorderPass client outcomes at 42% reflect how much file quality influences outcomes at this approval threshold.

The Philippines declined sharply despite being a stable market in 2024

From 51.8% to 33.9%, a near-18-point drop, DLIs that relied on the Philippines as a lower-risk alternative to African markets need to revisit that assumption.

China's Q4 dip warrants monitoring

After peaking at 62% in Q3, China dropped to 44% in Q4. The overall 2025 rate (55.6%) remains the highest of the five, but the year-over-year decline from 61.5% reflects the same tightening environment affecting all markets.

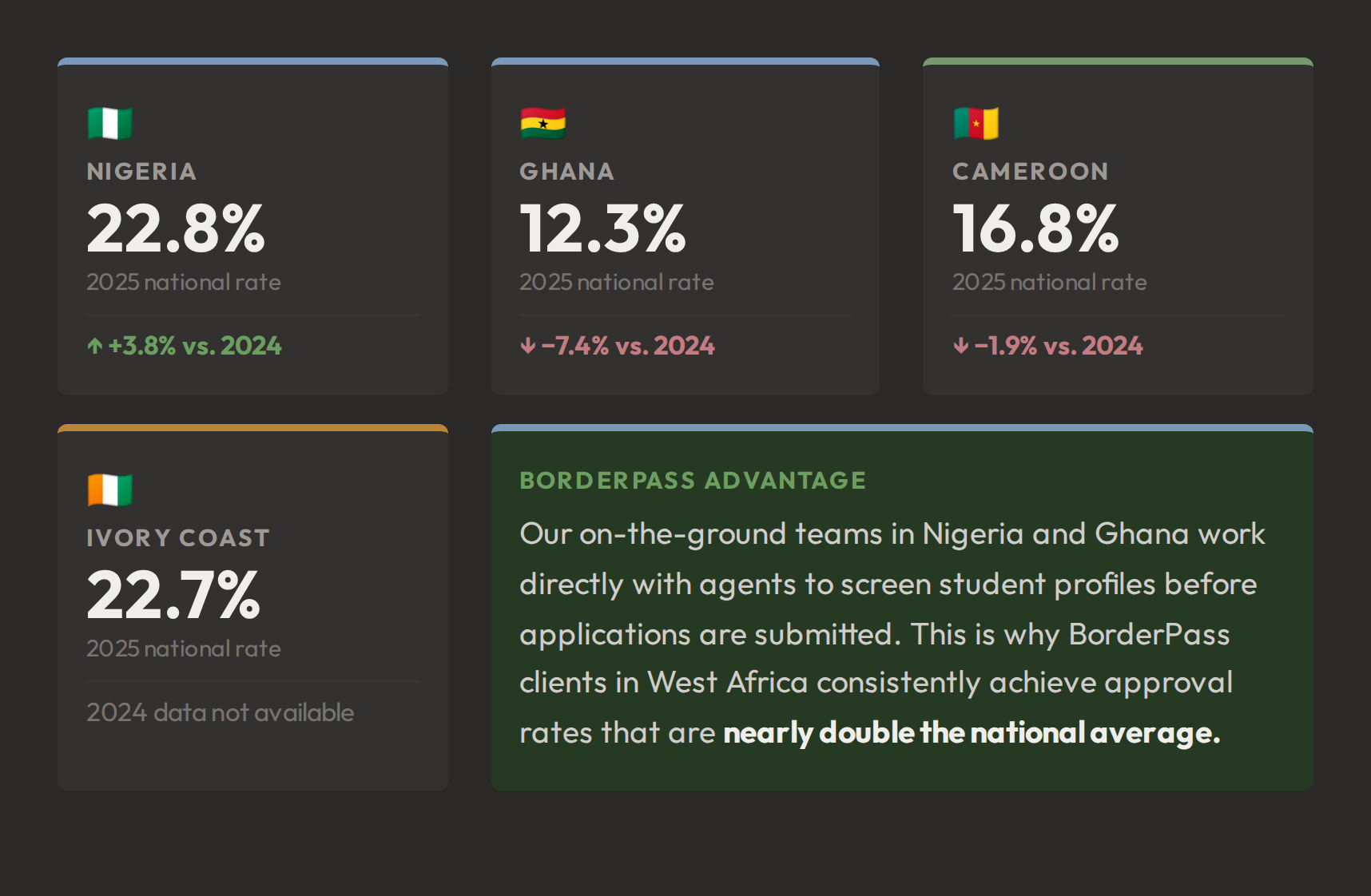

West Africa: The Most Complex and Consequential Market

West Africa represents one of the highest-volume sending regions for Canadian DLIs, and the most challenging approval environment globally. The region is not monolithic: Nigeria improved in 2025 while Senegal and Guinea experienced dramatic deterioration. Country-level distinctions are now essential.

The region is moving in different directions simultaneously. Nigeria improved, the only market in the top five to do so. Senegal collapsed 18.7 points, from 35.9% in 2024 to 17.2% in 2025. Guinea's near-total deterioration to 7.2% signals that IRCC has effectively closed one of the region's historically harder markets. Blanket regional strategies will not work, country-level targeting is now essential.

Nigeria is trending in the right direction

The national rate improved from 19.0% in 2024 to 22.8% in 2025, with steady quarterly performance throughout the year. BorderPass clients in Nigeria averaged 42%, nearly double the national rate, showing how much proper application support moves the needle.

Ghana improved through mid-year but gave back gains in Q4

Rates climbed from 4% in Q1 to 20% by Q3, then fell back to 12% in Q4. Ghana remains a workable market for DLIs with strong pre-screening processes in place.

Ivory Coast is worth watching as an emerging anglophone-adjacent market

At 22.7%, it tracked closely with Nigeria's rate in 2025. With a growing student population and rising interest in Canadian education, it represents a practical diversification option within the region.

A note on Latin America

Brazil (84.5%, up from 77.4% in 2024), Colombia (70.1%, up from 68%), and Mexico (60.3%) continue to significantly outperform on approval rates. For DLIs seeking to diversify away from West African risk concentration, Latin America offers consistently high approval outcomes with growing student interest in Canada. Watch for a dedicated BorderPass briefing on this market.

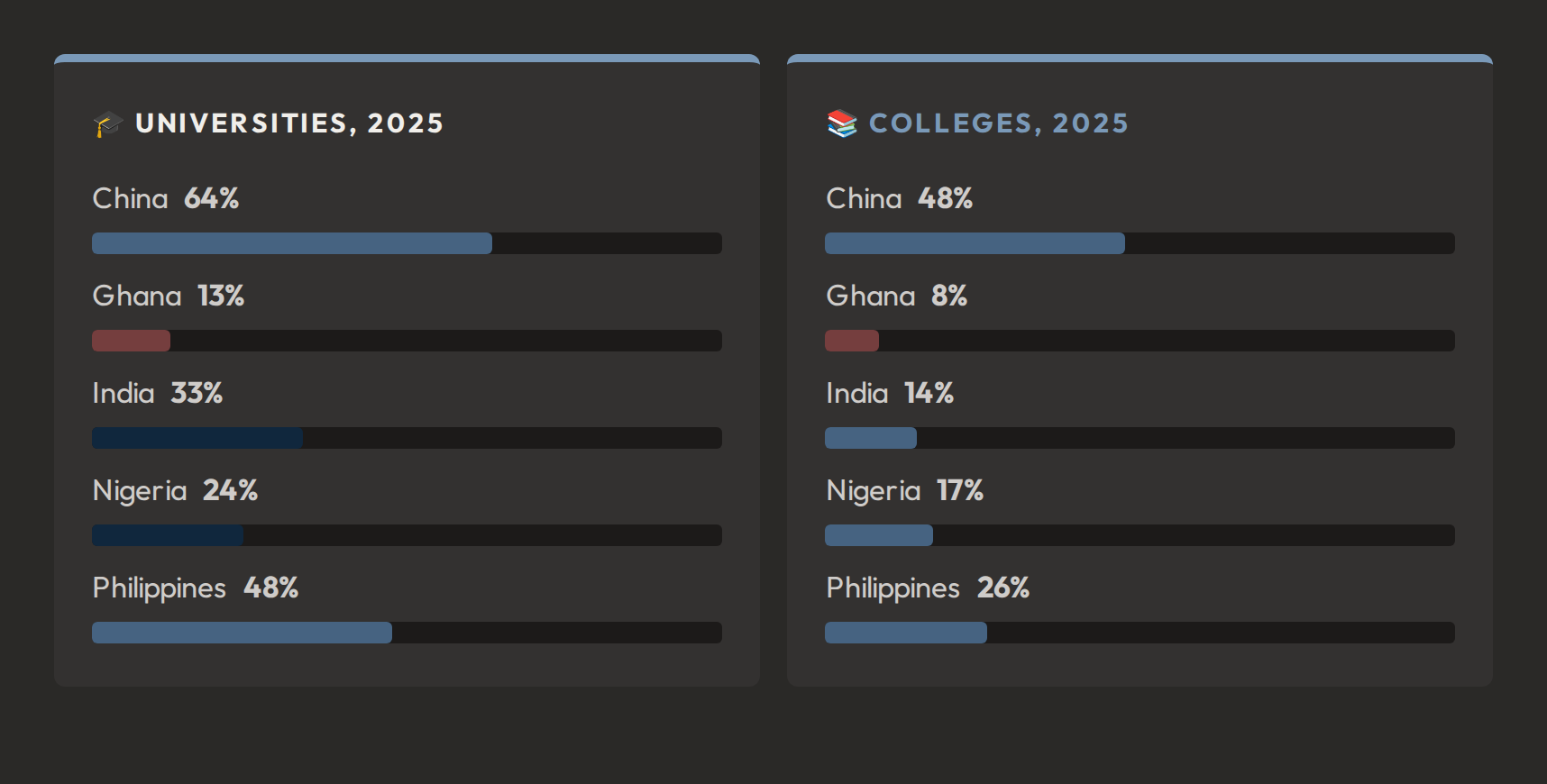

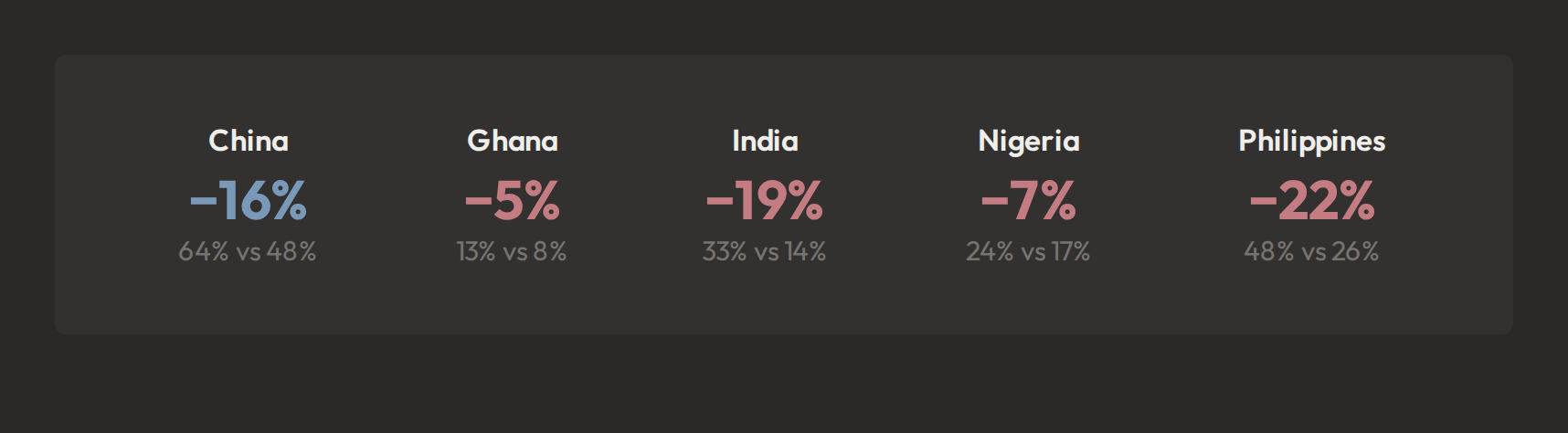

Universities vs. Colleges: A Persistent and Widening Gap

Across every key source country, university applicants consistently outperformed college applicants in 2025. The gap is most acute in India (19%) and the Philippines (22%). There is no key source country where college applicants match or exceed university approval rates.

India's 19-point college gap is the most critical finding for the college sector. College applicants from India were approved at just 14% in 2025, less than half the university rate of 33%. Combined with India's overall 41.7-point decline from 2024, this creates a compounding challenge for Ontario and BC colleges that historically relied on Indian enrollment. The pattern is consistent across every market: universities always outperform colleges. This is not noise, it is a systemic IRCC preference for program level that college-sector DLIs must actively address through file quality and student profile-building well before submission.

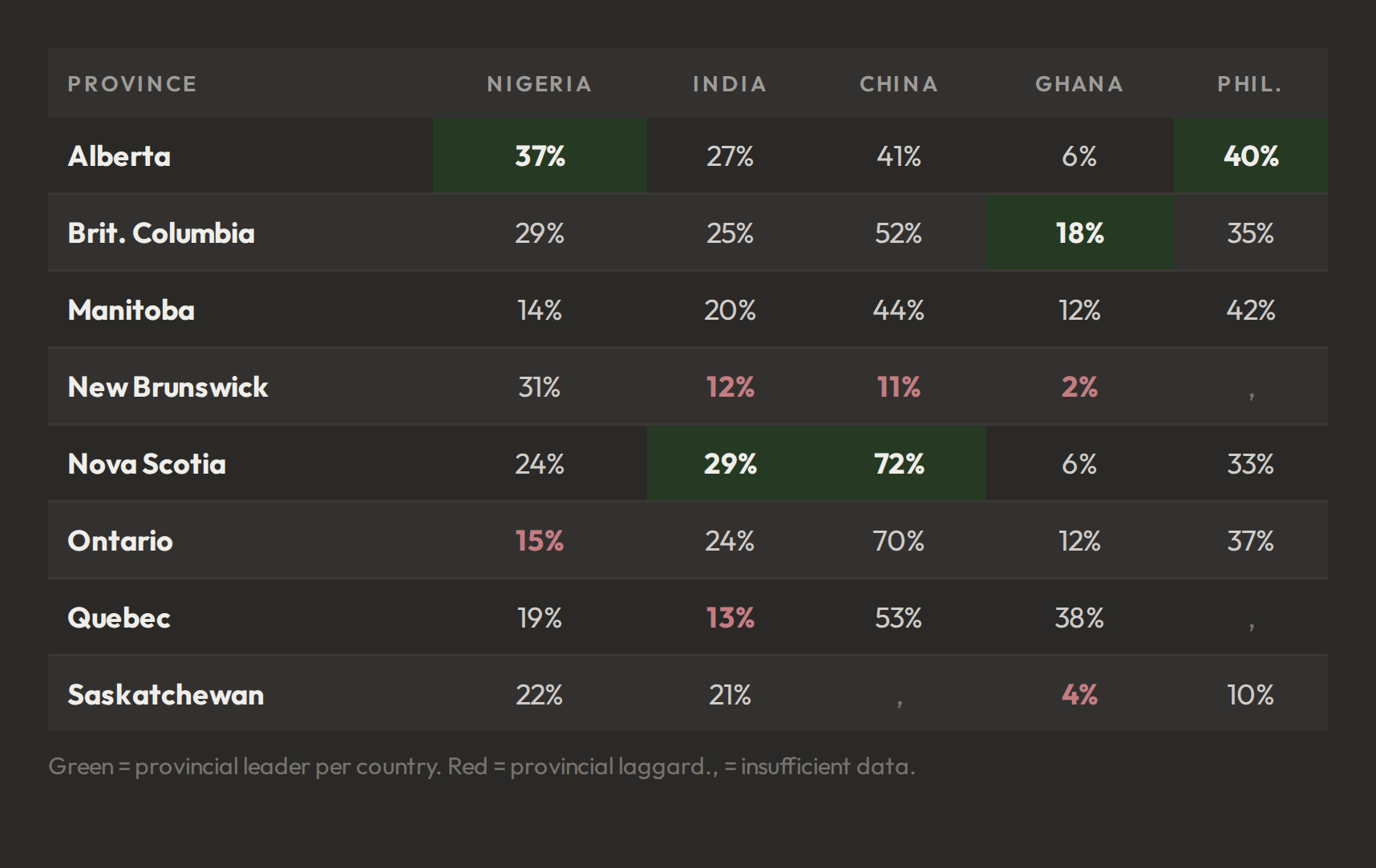

Province of Study: An Under-utilized Competitive Variable

Where a student applies to study can swing approval odds by 10–25 % for the same source country. This data is rarely communicated in agent briefings, and represents an under-utilized advantage for DLIs in provinces with stronger approval profiles.

Alberta leads for Nigerian applicants at 37%, more than double Ontario's 15%

Alberta-based DLIs have a communicable advantage in the West African market that should feature in agent briefings and student-facing materials.

Nova Scotia outperforms its size on multiple markets

29% for India and 72% for China, the highest of any province, make Nova Scotia DLIs particularly well-positioned for Chinese and Indian recruitment. These figures should be front and centre in institutional marketing.

Ontario's Nigeria rate of 15% is a systemic challenge

Ontario hosts the largest concentration of Canadian DLIs, meaning this low figure directly constrains enrollment outcomes for the sector's largest providers and drags down the national average.

Quebec has a structural India problem at 13%

Among the lowest of any province, this figure needs to be reflected in expectation-setting and application support resourcing for Quebec DLIs investing in Indian recruitment.

What 2025 Tells Us About the Environment Ahead

The 2026 Auditor General's Report, tabled March 23, 2026, and accepted by IRCC Minister Lena Metlege Diab, signals a clear shift: Canada is moving from a volume-based model to one defined by quality, oversight, and accountability.

The Auditor General found 50 DLIs failed to file enrollment compliance reports in 2025, representing 10,000 students, and IRCC imposed no consequences. That is about to change. Minister Diab has accepted recommendations to strengthen enforcement, including potential suspensions of up to one year for non-compliant institutions.

IRCC has set the 2026 study permit cap at 408,000, a further 7% reduction from 2025. With extensions again projected to dominate cap space, the realistic pipeline for new international students continues to shrink. DLIs planning around headline cap numbers will continue to be caught short.

The AG report calls for alignment with regional labour market needs, particularly STEM and Healthcare. DLIs whose programs credibly map to these priorities, and who can demonstrate graduate workforce outcomes, will be better positioned in the new regulatory environment.

With India and Nigeria both below 30% national approval rates, and the Philippines declining sharply, concentration in these markets carries compounding risk. Latin America, Vietnam (61.4%), and Kenya (39.3%) offer diversification paths with significantly better approval profiles.

Coming soon: BorderPass will be publishing a full analysis of the 2026 Auditor General's Report and its implications for DLI compliance, PAL strategy, and enrolment reporting.

Built for the Environment DLIs Are Now Operating In

In an environment defined by lower caps, stricter compliance requirements, and approval rates that vary dramatically by source country, institution type, and province, the margin for error has never been narrower. Institutions that come out ahead will be those with the best data, the strongest application infrastructure, and the deepest on-the-ground intelligence.

Screen immigration profiles before admission, track applications in real-time, and forecast final enrollment with live analytics, from inquiry to arrival.

Physical teams on the ground in Africa and India provide direct support for your in-country reps and agent networks, elevating quality at the source.

By filtering for quality early, we protect your PAL allocation and convert more Letters of Acceptance into enrolled, compliant students.

Book a Strategy Call

Connect with the BorderPass team to discuss how your institution's source market strategy can be optimized for the 2026 landscape. Click here to book a strategy call with our team.